I’ve learned that you have to be very thick-skinned to be a trader or a blogger. Many of my blogs are lifted directly from the pages of my old trading journals, and as I write about these former trades, I am very conscious not to sugar-coat it or make it look better than it actually was.

I’ve learned that you have to be very thick-skinned to be a trader or a blogger. Many of my blogs are lifted directly from the pages of my old trading journals, and as I write about these former trades, I am very conscious not to sugar-coat it or make it look better than it actually was.

This week, I’ll describe how I slipped right into a rather expensive trading mistake. At the same time, I’ll also tell you that I paid my tuition to the market, that I only did this misstep once and that I’ve learned from this mistake. I’ll explain what happened in detail, but let me also add that despite this specific instance of being tutored in the mutual fund arena, the lesson has been carried over to the stock arena and ETF arena as well. More on that later.

Let me take you back to the years 2003 – 2006. The market had a strong, 85%-plus run, and in April 2006, it hit a high followed by a normal 8% pullback. By late October of 2006, it took out the April high and was moving strongly into November. I fell prey to an overly-excited state of mind and made a bad, impulsive decision during open market hours. Normally, my strategizing is done when the markets are closed, which I’ve found offers me more clarity and tension-free reviews of my data points, information sources and charts. On that day, my mistake was rushing a sizeable mutual fund buy without doing my normal due diligence and preparation. Then pow… four days later, I received a humongous distribution which resulted in a pretty nice gift for Uncle Sam. By investing at the wrong moment, I essentially was handed back a large portion of my investment as taxable capital gains with an untended large tax liability.

- Impulsive trading must be curbed – always.

- Mutual fund distributions tend to be on a regular cyclical calendar so that the past generally does predict the future for the most part as to when distributions occur.

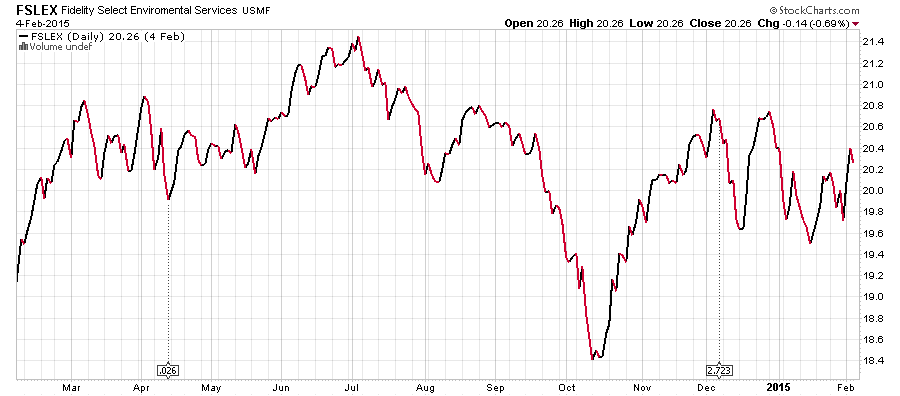

- An important part of any due diligence is to monitor portfolio manager changes. If you have new managers (as did FSLEX), the probability is that they will dump the previous managers’ holdings which will trigger loads of capital gains. In the chart below, if you bought FSLEX on December 3rd for $20.76, two days later you would have received a distribution of $2.73. Now you owe the government a portion of the funds you’d just barely invested.

- Distribution dates should be saved on all your chart styles and closely monitored before executing any buys or sells. The chart style you save and use for mutual funds should show historical distributions (use the overlays menu and pull-down events).

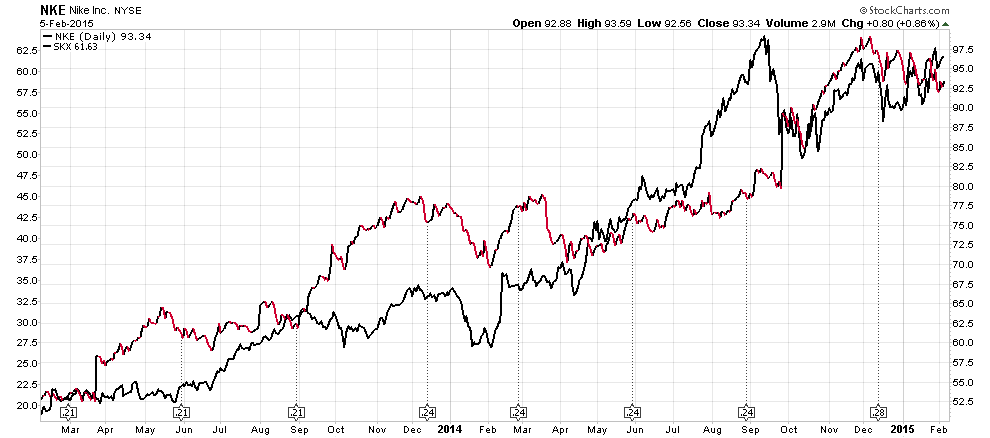

As I mentioned earlier, I paid my tuition in the mutual fund arena, but was able to apply similar lessons learned to the stock arena. First, an important caveat about the limitations of stock charts and dividend yields. FACT: Price charts do not reflect dividends. In my example below, Nike (NIKE) and Skechers (SKX) are in similar businesses and have performed somewhat the same over the past couple of years. That would be your conclusion if you plotted both stocks on a performance chart and forgot or did not know that Nike pays you $0.28 per share every quarter in the form of a dividend. Skechers pays nothing. Do the math yourself to be convinced. Dividends often comprise a significant portion of many stocks’ returns, but are not reflected on price charts, therefore you use the overlay pull-down menu called events.

Having said that, it’s important to plot dividends for another reason. The timing of your buy or sell can impact your receipt of any dividend payments. StockCharts.com only reflects the date paid. You need to understand all four dates as they pertain to dividends. Here is a hypothetical example:

- Declaration Date – e.g. July 27, 2015. This is the date company XYZ announces that it will pay a dividend on a future date, called the Record Date – e.g. September 14, 2015. This sets a date when you must be on the company’s books as a shareholder in order to receive this dividend.

- Ex-Dividend Date – e.g. August 12, 2015. Once the company sets the date, the stock exchanges fix the ex-dividend date. Normally, it’s a couple of days before the Record Date. If you buy the stock on or after this date, you will not receive the dividend. The seller gets the dividend instead.

- Record Date – e.g. August 14, 2105. Shareholders of record on the company’s books on or before August 14th are entitled to the dividend.

- Payable Date – e.g. September 14, 2015. Just like it sounds – this is the date that dividends are paid and are shown as distributions on StockCharts.

The bottom line: Know your dates. With large dividends, the price of a stock may move up significantly as the ex-dividend date approaches and it may fall by that amount after the ex-dividend date. Learn these dates. Consider this simply part of the “language of the market” and understand it. It’s silly not to do so and will cost you if you don’t.

Hopefully, I have managed to hook you on the benefits of tracking distributions for your stocks and mutual funds. With ETFs, most investors believe they are all tax-efficient because that is how they have been marketed. These are the investors who will get an unexpected surprise when bitten by a much-hated capital gains distribution and then wonder what hit them.

All ETFs may be susceptible to some distributions because when funds collect dividend income or sell securities at a gain, they have to pay out the resulting income to shareholders in the form of a distribution. Usually, this occurs on a regular predictable annual calendar. If you buy an ETF right before they make these distributions, you’ll suffer an immediate tax hit. I think it’s unfair since you are paying taxes but didn’t get the full benefit from those gains. I’ll save the rant about unfair taxes for another blog, but let me focus on empowering you to pay less taxes by monitoring these historical distribution dates.

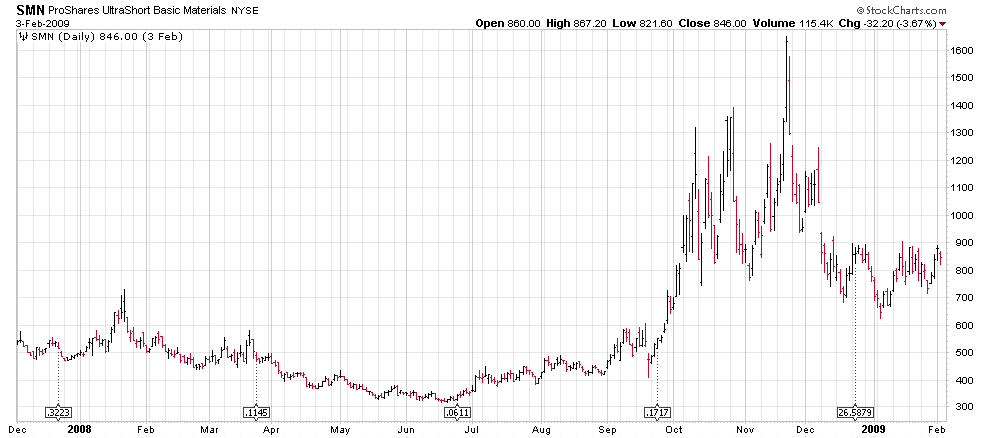

With respect to distributions, the worst offenders are derivative-based ETFs, such as ProShares UltraShort Basic Materials (SMN). Not to pick on SMN, but simply to use it as an example. As a general rule, I don’t suggest that investors buy leveraged ETF funds. As a hard and fast rule, I strongly urge you not to buy and hold these derivative-based leverage funds long term. They are intended for short term trading and because of their derivative-based strategy, they can generate huge and painful taxable distributions.

The bottom line is don’t sleepwalk through purchases of stocks, ETFs or mutual funds. Beware of past distribution dates so you are never surprised by today’s taxable distributions that haven’t benefitted you. StockCharts.com has made it easy to monitor these distributions so there really is no excuse to let Wall Street throw a pie in your face. Remember that monitoring distributions puts money in your pocket. As Nike says, “just do it!”

Trade well; trade with discipline!

-- Gatis Roze