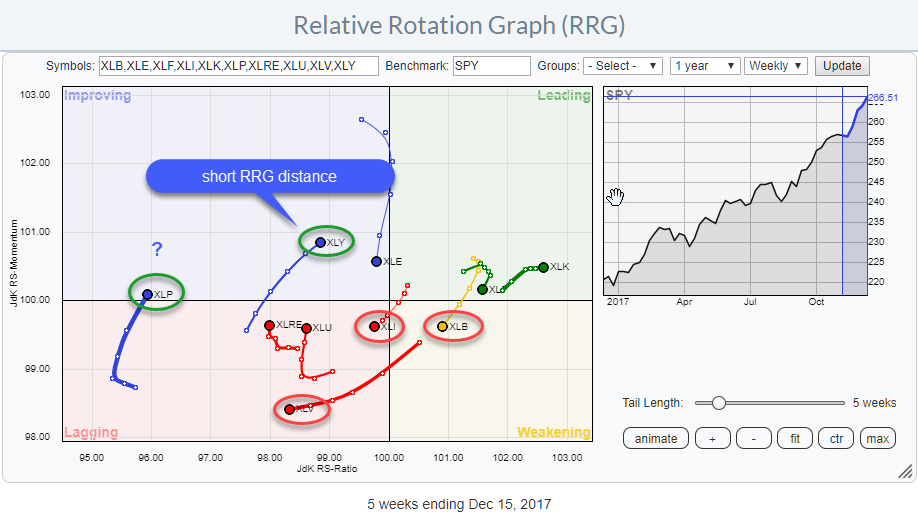

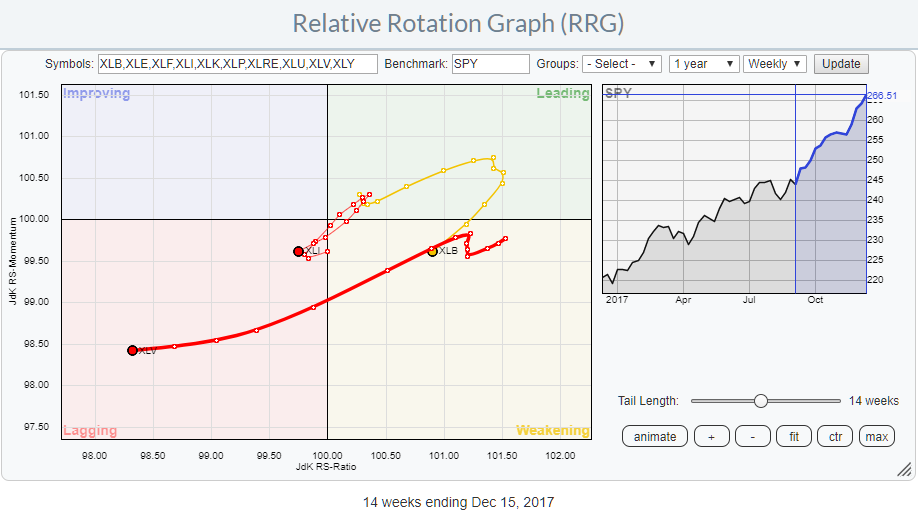

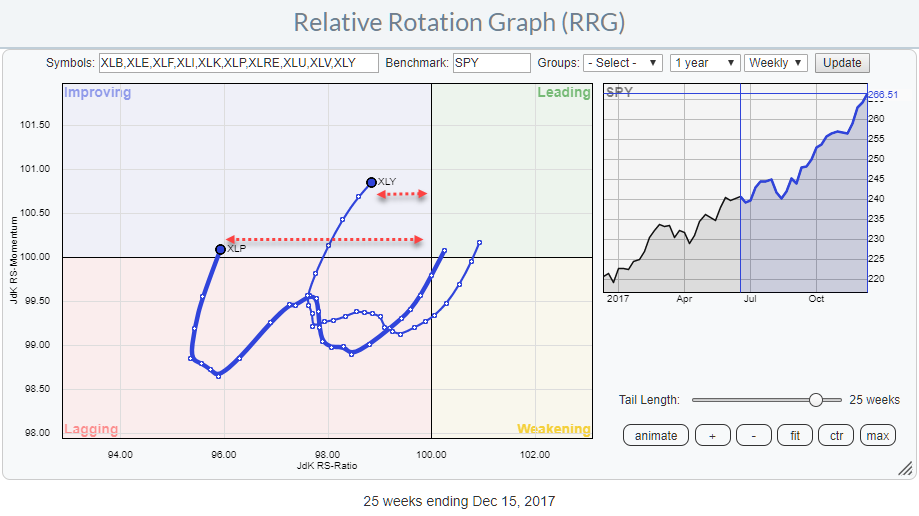

The Relative Rotation Graph for US sectors is showing us three sectors to avoid but also two which may offer good potential.

Inside the leading quadrant, we find XLK and XLF still being the strongest sector in US equity market based on their JdK RS-Ratio reading.

Energy (XLE) started heading due South almost immediately after entering the leading quadrant and now even turned back into improving while very close to the center (benchmark) of the RRG.

XLRE (Real Estate) and XLU (Utilities) are inside lagging but heading upward on the JdK RS-Momentum scale. Short tail lengths and weak price and relative charts in combination with the position on the RRG make me cautious for them.

Interesting enough both consumer sectors, Discretionary and Staples, are showing interesting rotations into the improving quadrant.

A very cautious approach is needed for XLV and XLI heading inside lagging and the same for XLB while it is still in weakening.

Summary

- Financials and Technology holding up well inside the leading quadrant supporting a stronger SPY

- Health Care expected to underperform in coming weeks

- Materials and Industrials provide unclear picture and are better avoided

- Both consumer sectors inside improving quadrant but RRG prefers XLY over XLP going forward.

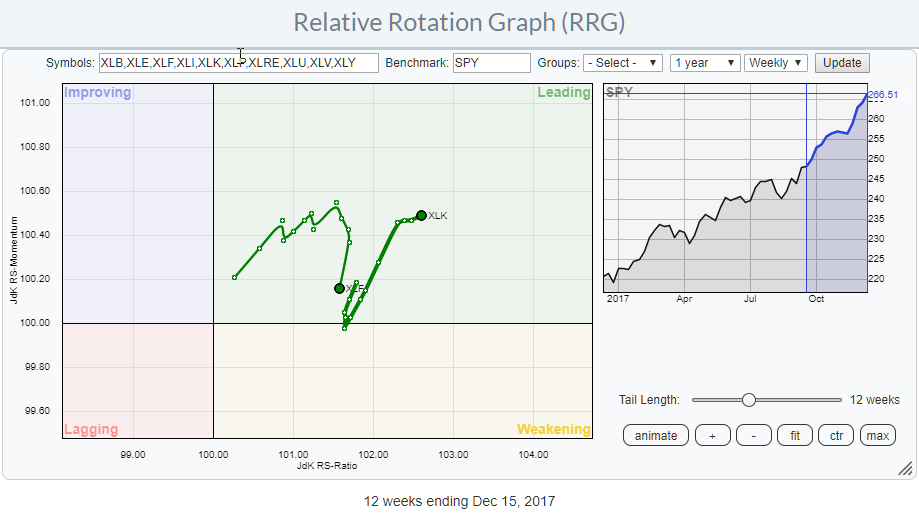

Two sectors in the leading quadrant

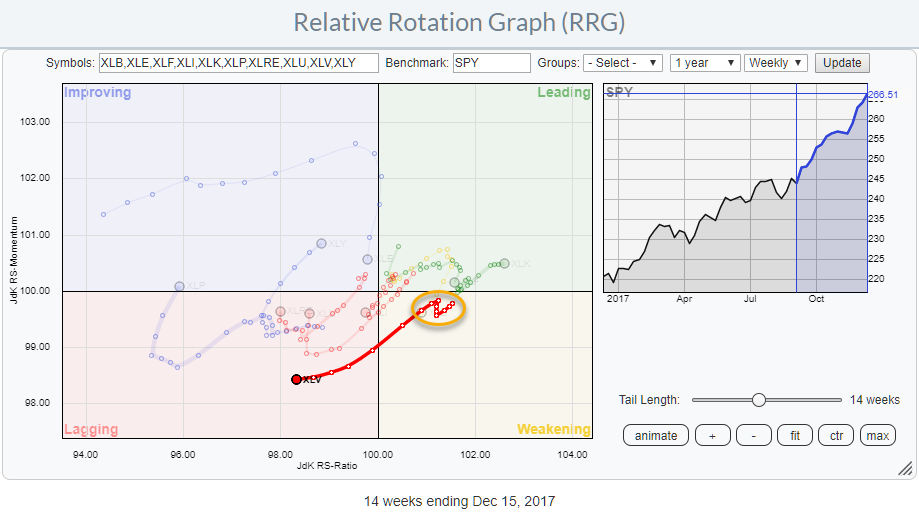

On most RRGs, we see a more or less evenly spread of the securities on the chart around the benchmark. For this group of US sectors, the picture seems to have shifted to the left. With four sectors in lagging and three in improving and only two in leading and one in weakening.

As this universe is a so-called "closed universe," which means that 100% of the benchmark is covered by the securities on the graph, we can get some additional information from this picture.

Together all the ETFs on this RRG make up the S&P 500 index. Mathematically this means that all distances measured from the benchmark, corrected for weight in the benchmark, to the positions of the various sectors (left and below 100 is negative) on the plot have to add up to zero.

With the two biggest sectors, Information Technology (24%) and Financials (15%), inside the leading quadrant, it means that we need more sectors on the left-hand side to keep the scale in balance.

From an analytical point of view, this means that we have to keep a close eye on the developments in those sectors to make a call on the general market (SPY) as they are likely to have a big impact.

For the time being, both sectors are still inside the leading quadrant which means that their relative trend against SPY is still up.

XLK is also still pointing higher on the JdK RS-Momentum scale, albeit minimal, while XLF recently started to lose some relative momentum. Being the number one and number two sectors within the S&P 500, based on JdK RS-Ratio, we have to judge this as temporary for the time being but keep a close eye in case the rotations start to pick up steam and move towards or into weakening.

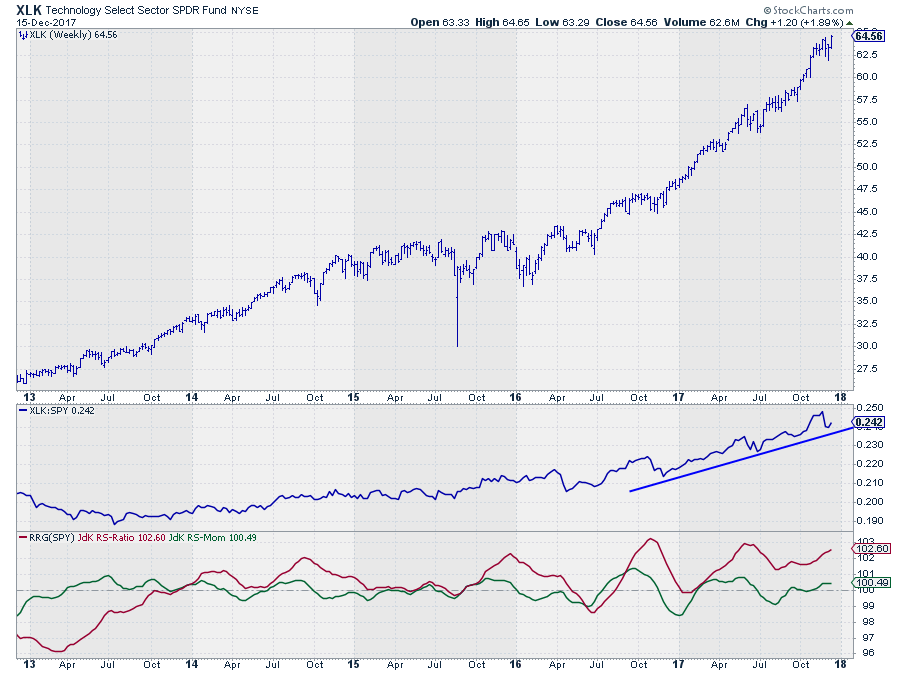

Technology select SPDR - XLK

The Rotation for XLK on the RRG chart is still heading higher on both scales, and its position highest on the RS-Ratio scale make it the strongest sector in the S&P 500.

The price chart is showing a strong uptrend with a very regular series of higher highs and higher lows just pushing to new highs last week.

The raw RS-Line did not make it to new highs yet but the trend, here as well, is undeniably up putting both RRG Lines above 100.

Until the rotational pattern for XLK starts to change there are no reasons to reduce any holdings at a sector level.

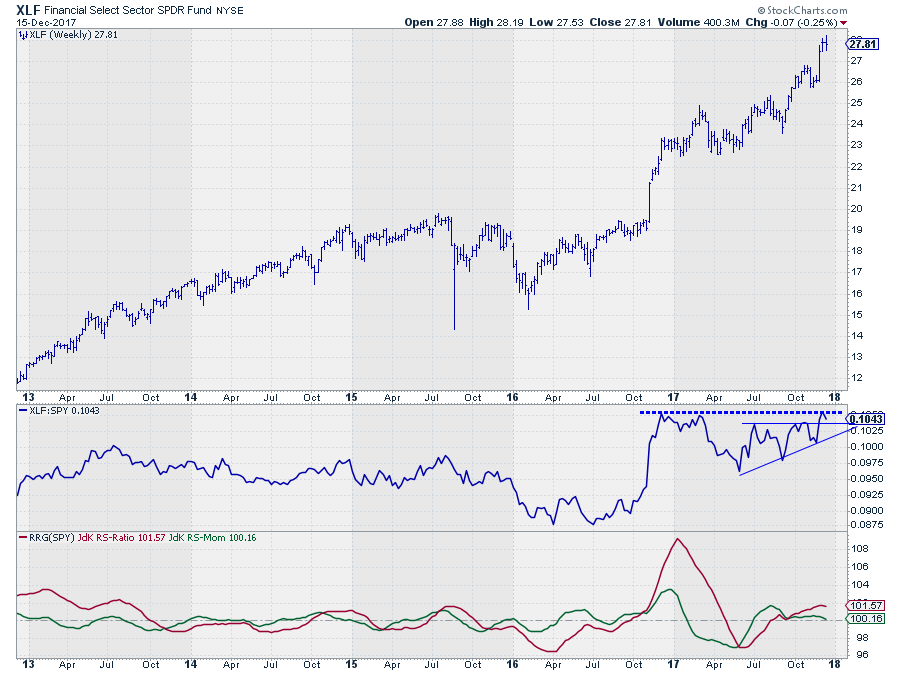

Financial Select Sector SPDR - XLF

The rotational pattern for Financials is a bit weaker than for Technology. The JdK RS-Momentum line has started to roll over a few weeks ago which causes the RRG-Heading to point in a South-Western direction. As the RS-Ratio is still well above 100, it is not alarming yet, but it indicates some short-term weakness.

Only when this short-term weakness continues and pushes the sector into the weakening quadrant and heading towards lagging, I will be more concerned.

If XLF can take out the old highs on the relative strength chart a very quick rotation back to a strong RRG-Heading is likely, and we can see more relative (out) performance from XLF.

Three sectors to avoid

Based on the rotational pattern on the Relative Rotation Graph for US sectors there are now three sectors that are likely to (continue to) continue to underperform the benchmark (SPY).

These are XLI which completed a sharp rotation close to the benchmark and is now starting to head deeper into the lagging quadrant. XLB which turned around inside leading and then moved into the weakening quadrant at a negative RRG-Heading.

And finally, XLV which is furthest into the lagging quadrant already and backed by one of the longest tails in this universe.

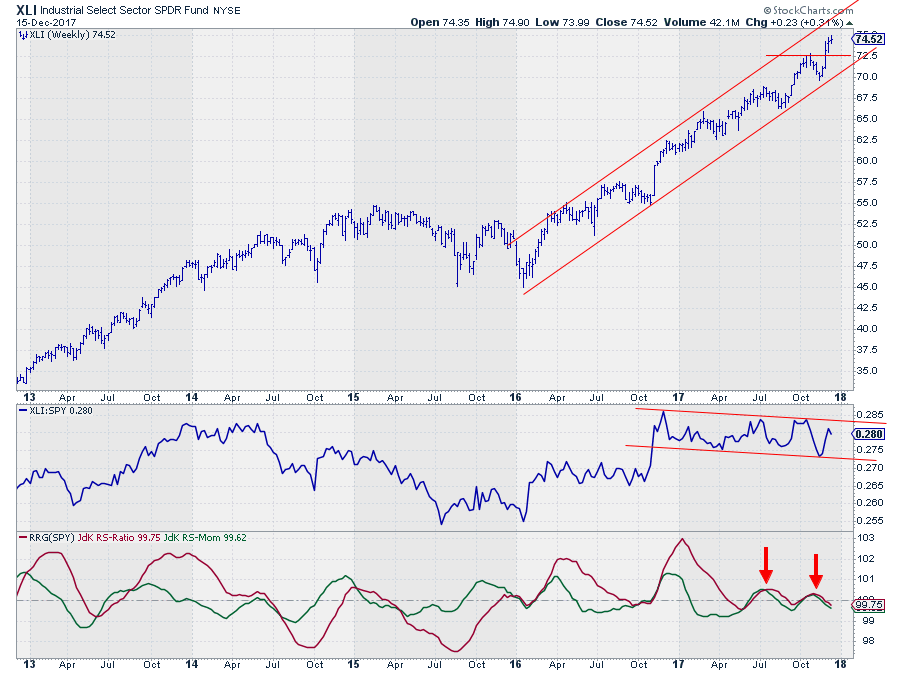

Industrial Select Sector SPDR - XLI

Industrials is showing a sharply rotating pattern around the benchmark recently (last 14 weeks as displayed on RRG above). This indicates a relative trend/performance in line with the benchmark.

We can check this in the table below the RRG (click the live version) where we find that XLI's performance over the past 13 weeks was 10.2% versus 9.2% for SPY.

On the price- in combination with the relative charts this is seen as the RRG-Lines oscillating close to and around the 100-level, which is the result of the RS-Line trading sideways in a slightly down-sloping range.

On the Relative Rotation Graph, XLI is now clearly pointing into the lagging quadrant at a negative RRG-Heading but still close to the benchmark.

The rotational pattern, in combination with the relative lines, is negative but the price chart is still showing a lot of strength and just pushed to a new high. I am avoiding XLI for overweight or long positions with these conflicting signals but also not ready to be very negative yet.

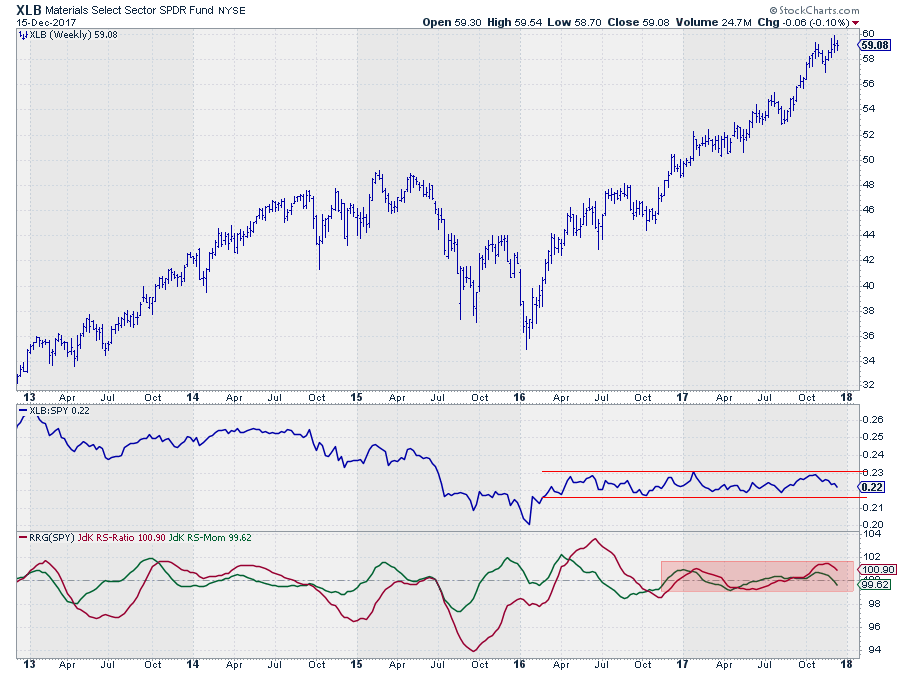

Materials Select Sector SPDR - XLB

Out of the three sectors to avoid, Materials is the only one still inside the weakening quadrant. The rotational pattern is a bit wider than we saw for XLI but not much and it can still be qualified as "close to the benchmark" especially compared to the other rotations that are visible on the RRG.

Here also the RS-Line is trading in a very narrow range, already since early 2016, resulting in RRG-Lines that are oscillating around the benchmark.

The catalyst for a bigger and more directional move, from a relative point of view, will be a break of relative strength out of that sideways range. Until that happens rotations on the RRG will remain close to the center of the chart and offer little opportunity to add alpha to a portfolio.

With the RRG-Heading now negative this makes XLB a sector to avoid even for shorter-term positions.

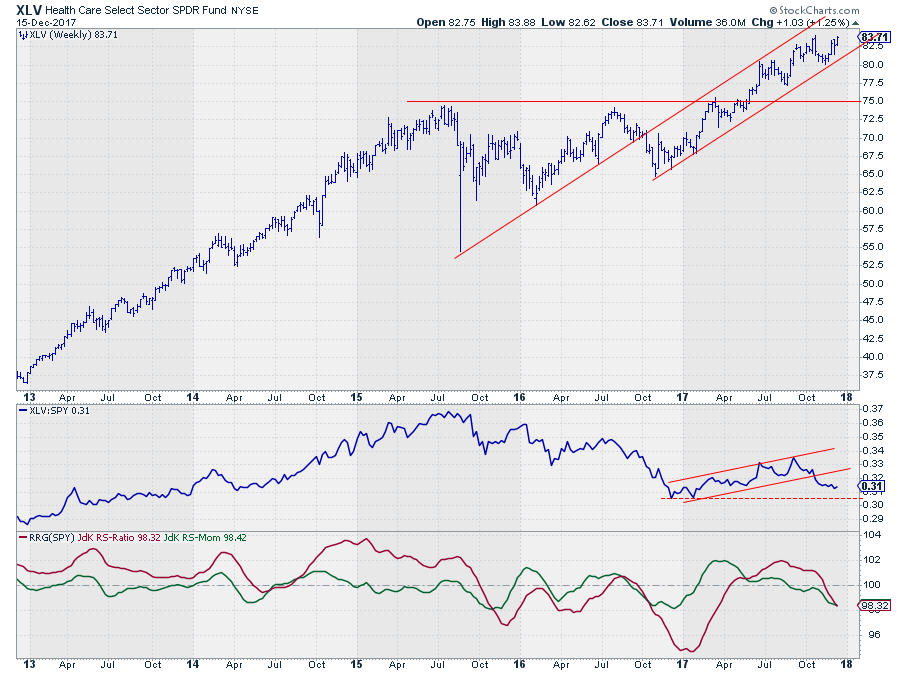

Health Care Select Sector SPDR - XLV

The Health Care sector is the one with the longest tail and accelerating into the lagging quadrant over the past weeks. This makes it a very vulnerable sector.

It is the sector with the weakest JdK RS-Momentum reading while pointing at an RRG-Heading around 260 (almost due West).

Look at the observations inside the orange oval being very close together during a period when not much happened in the relative trend. Then all of a sudden the tail starts to pick up steam and move away from that consolidation heading for the lagging quadrant. This is a good example where the increasing distance between RRG data-points on the tail indicates an acceleration into a more directional move.

The break below support in relative strength and the fact that this is one of the few sectors that has not managed to push to new highs recently makes Health Care a dangerous sector for the moment with more downside potential (relative) ahead.

From a relative perspective, the upside potential is now limited to the level of the former support line which will act as resistance on the way up. Any relative recovery in combination with a failure to break to new highs is regarded as an opportunity to reduce any Health Care holdings or profit from a renewed acceleration in the relative downtrend.

Watch the two consumer sectors.

Inside the improving quadrant, we find both consumer sectors at more or less the same RRG-Heading. The big difference between Staples (XLP) and Discretionary (XLY) is their position on the Relative Rotation Graph.

Theoretically, these two sectors should be moving/rotating more or less opposite of each other. They use to serve well as a risk-on / risk-off indicator. This is now a bit more difficult to read with both trails tracking a similar rotation.

Just to be clear from the start, BOTH sectors look good for the time being and at both seem ready for at least a short period (weeks) of outperforming SPY. If this short-term improvement will turn into a turnaround of their relative downtrends remains to be seen.

The analysis of the two sectors below is an attempt to get a preference between the two.

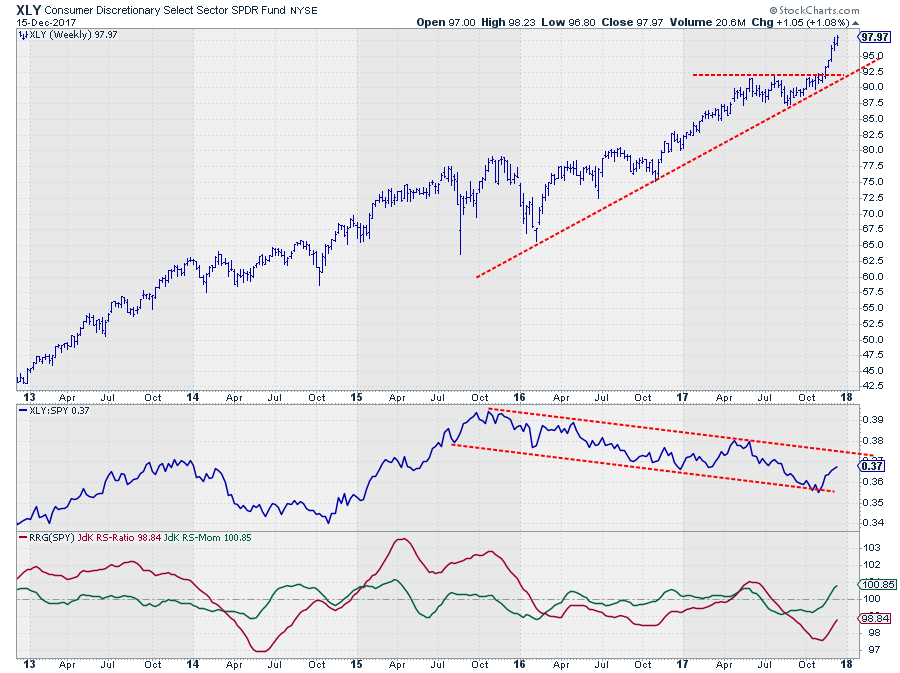

Consumer Discretionary Select Sector SPDR - XLY

The weekly bar chart of Consumer Discretionary (XLY) is still showing a strong uptrend. The recent break above horizontal resistance around 92.50 once again confirmed this strength. From a price perspective, this is a strong chart.

The relative picture is different. Relative Strength is in a downtrend since late 2015 and as of now still moving lower within the boundaries of the falling channel.

From a relative perspective, this is, therefore, still a recovery in a downtrend which makes it questionable if XLY will be able to continue its recent rotation into the leading quadrant and turn around the current relative downtrend.

What makes me still a bit cautious is the shortening of the distances between the observations on the weekly tail for XLY. This indicates a slow down in the rotation.

A break out of the falling channel on the relative strength line accompanied by a break above 100 for the JdK RS-Ratio line and an acceleration in the rotation will make XLY a sector with a lot of upside potential pushing into the leading quadrant.

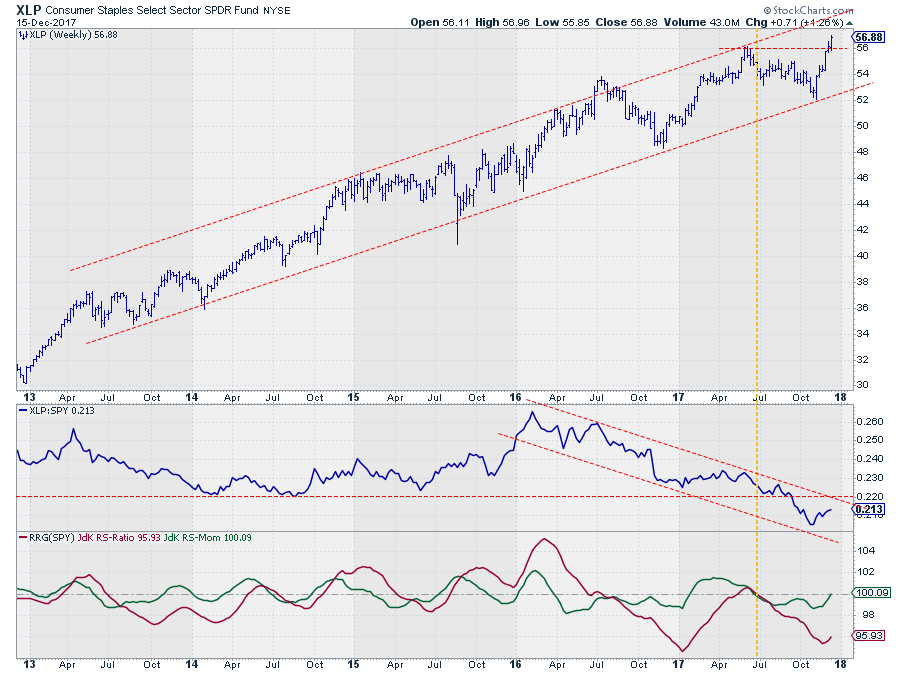

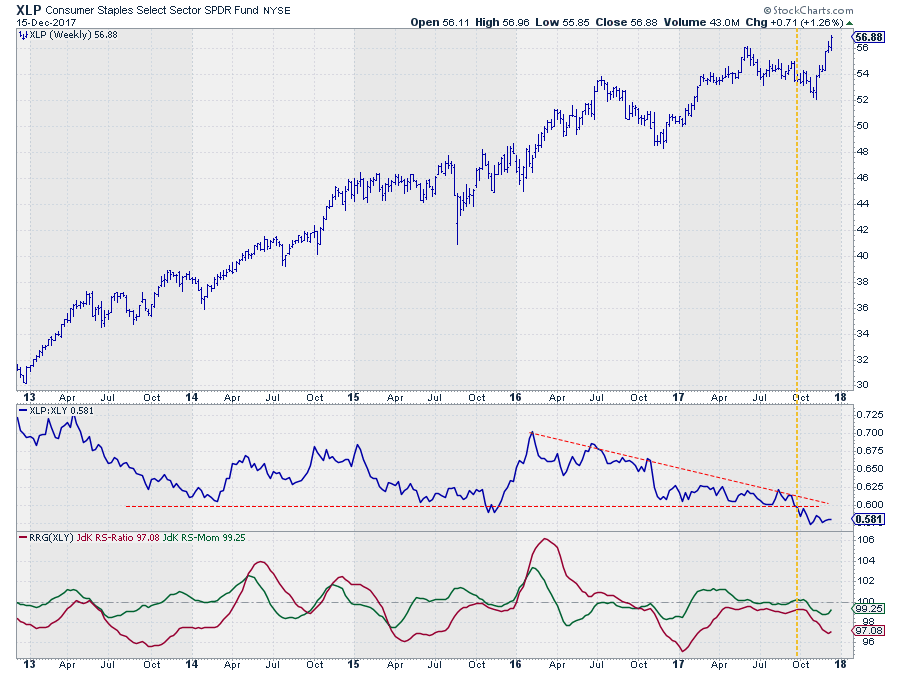

Consumer Staples Select Sector SPDR - XLP

Here also the price chart is showing an uptrend that just got confirmed by a break to new highs.

The rotational picture for the other consumer sector, staples, is largely similar but wider and further away from the center of the chart. This indicates that both have underperformed the benchmark, but XLP was the weaker of the two.

Again this can be checked in the table below the RRG. Over the past 25 weeks (6 months) XLP gained only 5.5% while XLY gained 11%. Both, however, underperformed SPY which rose 12.1%.

For XLP, also, it will be important to break out of the falling channel on the RS-line and push both RRG-Lines above 100 to turn around the relative downtrend. Until then here also the rotation has to be judged as a recovery within the existing downtrend.

Looking at the distances between the observations on the XLP tail we see a difference with XLY. On the XLP tail, the distances are growing, indicating that the rotation is accelerating. This indicates that for the next few weeks XLP may be moving faster (better) than XLY.

Staples vs Discretionary

The final comparison is a straight RS-line between Staples and Discretionary. The break below support late September signaled more weakness for XLP vs. XLY, and this situation is still ongoing. The subsequent decline has pushed both RRG-Lines lower indicating a clear preference for Discretionary over Staples.

The small uptick that is visible in both the RS-Ratio and the RS-Momentum lines causes the increasing distances on the XLP tail indicating a very short-term improvement for Staples. From an RS-perspective this may translate in an uptick towards the former breakout level after which the decline continues, and the XLP/XLY ratio drops further.

This means a preference for Consumer Discretionary over Staples for now, which in its turn suggests a risk-on situation, supporting a positive view on SPY and the two sectors inside the leading quadrant as it is very hard, not impossible, for SPY to rise without strong Financial and Technology sectors.

If you like to receive a notification anytime, a new article is posted on this RRG blog, please leave your email address and press the green "Notify Me!" button below this article.

Julius de Kempenaer | RRG Research

RRG, Relative Rotation Graphs, JdK RS-Ratio, and JdK RS-Momentum are registered TradeMarks of RRG Research

Follow RRG Research on social media:

If you want to discuss RRG with me on SCAN, please use my handle Julius_RRG so that I will get a notification