The InterContinental Exchange (ICE) has just rolled out a new futures contract called the NYSE FANG+™, based on the original four FANG stocks (Facebook, Amazon, Netflix, and Google) plus 6 others. The FANG term was originally coined by CNBC’s Jim Cramer. Some analysts are seeing this as a sign of peak excitement over the trendy tech stocks, akin to a magazine cover indication. While they may have a point, they are likely early in making this call.

The InterContinental Exchange (ICE) has just rolled out a new futures contract called the NYSE FANG+™, based on the original four FANG stocks (Facebook, Amazon, Netflix, and Google) plus 6 others. The FANG term was originally coined by CNBC’s Jim Cramer. Some analysts are seeing this as a sign of peak excitement over the trendy tech stocks, akin to a magazine cover indication. While they may have a point, they are likely early in making this call.

The ICE website describes the properties of the new futures contract, which is based on an equal weighting of the 10 stocks. That introductory article includes a comparison of their new FANG+ to other indices, showing the FANG+ portfolio to be clearly superior to the SP500, Nasdaq 100, and the SP500 Info Tech Index, or at least is the case since 9/19/14. They chose that date as a start point for comparison because that was when Alibaba (BABA) came public.

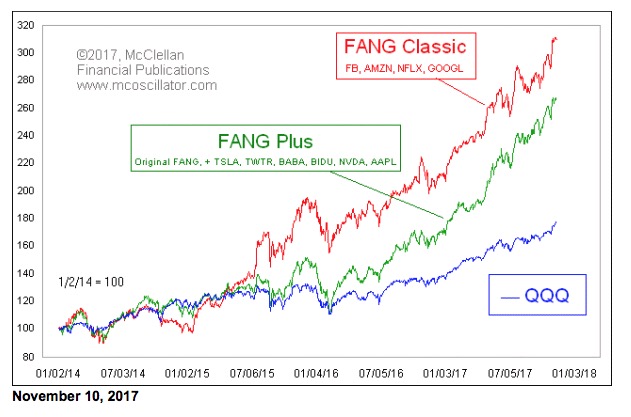

What their introductory article fails to mention is that the performance of the FANG+ portfolio actually is not as good as the original 4-stock FANG group. This week’s chart shows a comparison of the two portfolios since January 2014, with the FANG+ portfolio holding just the 9 stocks until BABA came public. And just for comparison, I have included the performance of QQQ.

The folks at ICE think that they are making a fancier product by including those 6 other trendy stocks (Tesla, Twitter, Alibaba, Baidu, Nvidia, and Apple), but their addition actually drags down the performance of the FANG group over the past 4 years. Whether their “improvement” will turn out to be an enhancement in the future remains to be seen, and depends on how those other 6 stocks do in the future.

What is clear in that chart above is that both of these FANG type indices are really just replicating the performance of the Nasdaq 100 Index (NDX), and its main ETF, QQQ, albeit with a performance kicker known as “beta”. The concept of a stock’s beta is that if its benchmark index moves up or down by 1%, then a stock should move by a multiple of that percentage, and the multiple is called the beta. So a stock with a beta of 2.0 would move 2% for every 1% move in its benchmark (in a perfect world).

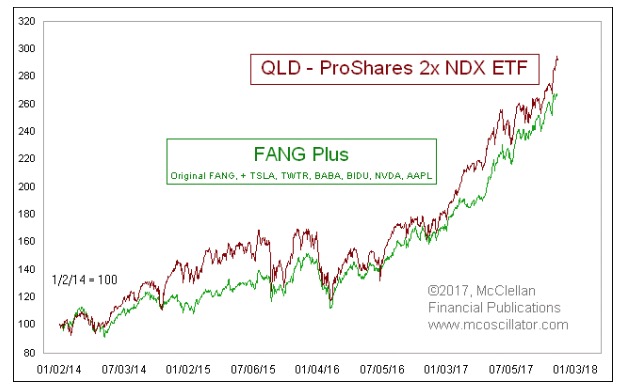

The ETF universe has come to embrace beta by inventing synthetic versions, using leverage to achieve multiples of the benchmarks’ performance. The ProShares fund family is among the better known providers of such products, and it has a 2x leveraged version of the NDX which trades under the symbol QLD. This next chart compares QLD to the performance of the FANG Plus stocks:

What it reveals is that the FANG Plus group of stocks really just replicates the performance of QLD very closely. So congratulations, ICE, you just invented a futures contract that replicates an already existing leveraged ETF.

Whether or not futures traders respond by displaying demand for this new futures contract remains to be seen. But the point for us to take away from this is that the FANG Plus product is not really anything new and different, just a repackaging of what was already available.

Tom McClellan

Editor

The McClellan Market Report

www.mcoscillator.com