Market Recap for Tuesday, November 14, 2017

For the third time in the last four days, we saw U.S. equities gap lower, only to reverse intraday to close near their highs of the session. It's still resulted in losses for the day, but it also shows the bull market resiliency that the bears are facing as they try to grab control of the near-term action. We're seeing fairly significant red futures once again this morning so the bulls will once again attempt to reclaim support by day's end.

All of our key indices finished lower on the session with the S&P 500 rallying to hold onto rising 20 day EMA support:

While the bulls continue to perform well in the very near-term, holding onto moving average support, don't lose sight of the fact that a negative divergence remains. That suggests we could see an upcoming 50 day SMA test. Don't rule it out.

While the bulls continue to perform well in the very near-term, holding onto moving average support, don't lose sight of the fact that a negative divergence remains. That suggests we could see an upcoming 50 day SMA test. Don't rule it out.

Defensive areas of the market continue to provide leadership during this consolidation phase as utilities (XLU, +1.25%) and consumer staples (+0.35%) were the two best performing sectors on Tuesday. Profit taking in energy (XLE, -1.62%) was problematic as crude oil ($WTIC) has fallen to test its recent $55 per barrel breakout.

Pre-Market Action

Economic reports will pick up, beginning with this morning. Already, we've seen inflation at the consumer level come in at expectations - a positive development after inflation at the producer level showed signs of heating up in yesterday's economic report. October retail sales also aligned very closely with expectations. Only the Empire State manufacturing survey disappointed. Its reading of 19.4 was solid, but fell short of 26.0 consensus estimates.

The 10 year treasury yield ($TNX) is down 6 basis points at last check to 2.32% and that sudden drop is not helping U.S. stock futures. Also not helping are global markets as we're seeing fairly significant selling pressure around the world overnight and this morning. Asian markets were weak with losses of 1% or more in both Tokyo and Hong Kong. In Europe this morning, the German DAX (featured in Current Outlook section below) was down nearly 1%, adding to a slide of approximately 500 points the past six trading days.

Dow Jones futures are down over 100 points (at last check) in sympathy as we approach today's opening bell.

Current Outlook

There's a very tight positive correlation between the performance of the benchmark S&P 500 ($SPX) and the German DAX ($DAX). They tend to take turns in leadership, but over time they have proven to follow one another. One issue the S&P 500 currently faces is that selling has quite suddenly taken over in Germany. Here's a current look at the DAX:

The 12900 level is fairly important on the DAX as the 50 day SMA is currently at 12864 and rising, price support resides closely to 12900, RSI has dipped into the 40s (typically a solid area of support during uptrends) and the first Fibonacci retracement support level (38.2%) is at 12887.

The 12900 level is fairly important on the DAX as the 50 day SMA is currently at 12864 and rising, price support resides closely to 12900, RSI has dipped into the 40s (typically a solid area of support during uptrends) and the first Fibonacci retracement support level (38.2%) is at 12887.

From a bullish perspective, we want to see the DAX reverse at its current level. Keep an eye on the DAX today.

Sector/Industry Watch

Unlike both financials (XLF) and industrials (XLI), the technology sector (XLK) did not suffer from slowing price momentum. Instead, the XLK simply became very stretched and overbought in the near-term. That's resulted in a need for consolidation and an unwinding of overbought conditions. That seems to be what's occurring now as the XLK's daily RSI has fallen from the mid-80s down to 70 at yesterday's close. Additional selling down to the rising 20 day EMA would not be a bad thing given the current technical state of the sector:

Following those huge advances (blue directional lines), we've seen a quick pullback (May) and two other more significant periods of consolidation (March-April, then June). Given the strength of the current daily momentum (MACD), I'd expect to see buying take place in technology if we see another 20 day EMA test (green arrows). The next price high, however, could see a negative divergence emerge. Such a development would significantly increase the risk of trading technology stocks. For now, I'd only look for relief from short-term overbought conditions.

Following those huge advances (blue directional lines), we've seen a quick pullback (May) and two other more significant periods of consolidation (March-April, then June). Given the strength of the current daily momentum (MACD), I'd expect to see buying take place in technology if we see another 20 day EMA test (green arrows). The next price high, however, could see a negative divergence emerge. Such a development would significantly increase the risk of trading technology stocks. For now, I'd only look for relief from short-term overbought conditions.

Historical Tendencies

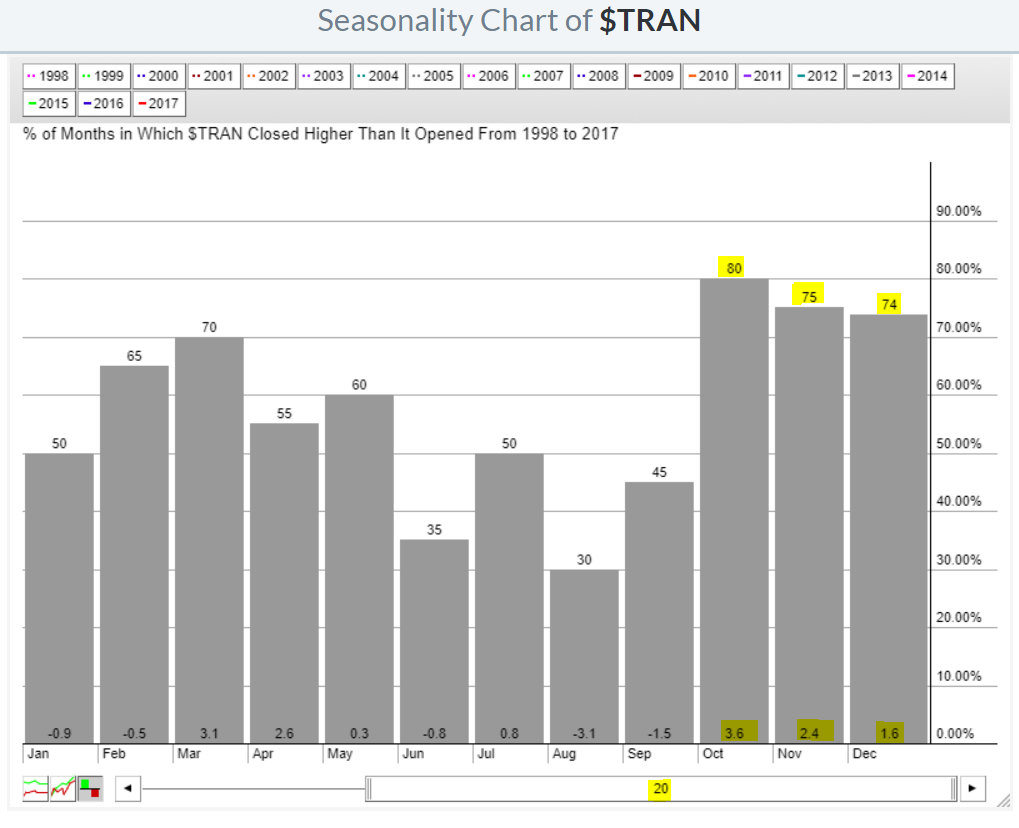

Yesterday, I pointed out that transportation stocks ($TRAN) were still hanging onto trendline support, despite the fact that this area of the market has been struggling for weeks. The seasonal chart below highlights that the TRAN typically performs its best in the fourth quarter of the year:

The yellow highlighted numbers at the top tell us the percentage that each month has moved higher over the past 20 years. For example, transportation stocks have gained ground 16 of the last 20 years (80%) during the month of October. That percentage is similar for both November and December. At the bottom of those columns, the highlighted numbers represent the average monthly gains for each of the three months. Clearly, the fourth quarter is the seasonal sweet spot for transports. In my opinion, this provides further evidence that transports will more likely than not hold their longer-term uptrend line and resume their earlier bullish tendencies.

The yellow highlighted numbers at the top tell us the percentage that each month has moved higher over the past 20 years. For example, transportation stocks have gained ground 16 of the last 20 years (80%) during the month of October. That percentage is similar for both November and December. At the bottom of those columns, the highlighted numbers represent the average monthly gains for each of the three months. Clearly, the fourth quarter is the seasonal sweet spot for transports. In my opinion, this provides further evidence that transports will more likely than not hold their longer-term uptrend line and resume their earlier bullish tendencies.

Key Earnings Reports

(actual vs. estimate):

TGT: .91 vs .86

(reports after close, estimate provided):

CSCO: .60

NTAP: .69

NTES: 3.04

Key Economic Reports

October CPI released at 8:30am EST: +0.1% (actual) vs. +0.1% (estimate)

October Core CPI released at 8:30am EST: +0.2% (actual) vs. +0.2% (estimate)

October retail sales released at 8:30am EST: +0.2% (actual) vs. +0.1% (estimate)

October retail sales, excluding autos, released at 8:30am EST: +0.1% (actual) vs. +0.2% (estimate)

November empire state manufacturing survey released at 8:30am EST: 19.4 (actual) vs. 26.0 (estimate)

September business inventories to be released at 10:00am EST: +0.1% (estimate)

Happy trading!

Tom